Use our IOU template to detail how borrowed money will be repaid.

Updated July 14, 2024

Written by Sara Hostelley | Reviewed by Brooke Davis

An IOU (I Owe You) is a legal document that sets out the details of a loan made between a borrower and a lender. The note clearly outlines the borrower’s commitment to fully repay the lender.

An IOU is a written debt acknowledgment form that includes a promise to repay the debt owed. This document recognizes a legally binding relationship between the borrower and the lender.

It includes the loan transaction’s terms and conditions and ensures the parties have a thorough written record of the deal and their intentions. The parties should finalize the note before any money changes hands.

An IOU allows both parties to record the borrowed money and clarify when the borrower should repay the loan. It’s useful for loans between family, friends, and colleagues and reminds the parties involved of the loan details.

Here are some everyday situations when parties might use this document:

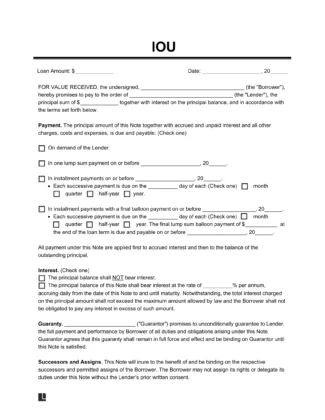

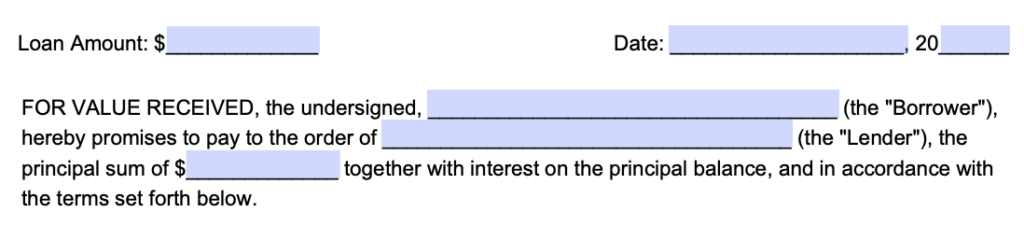

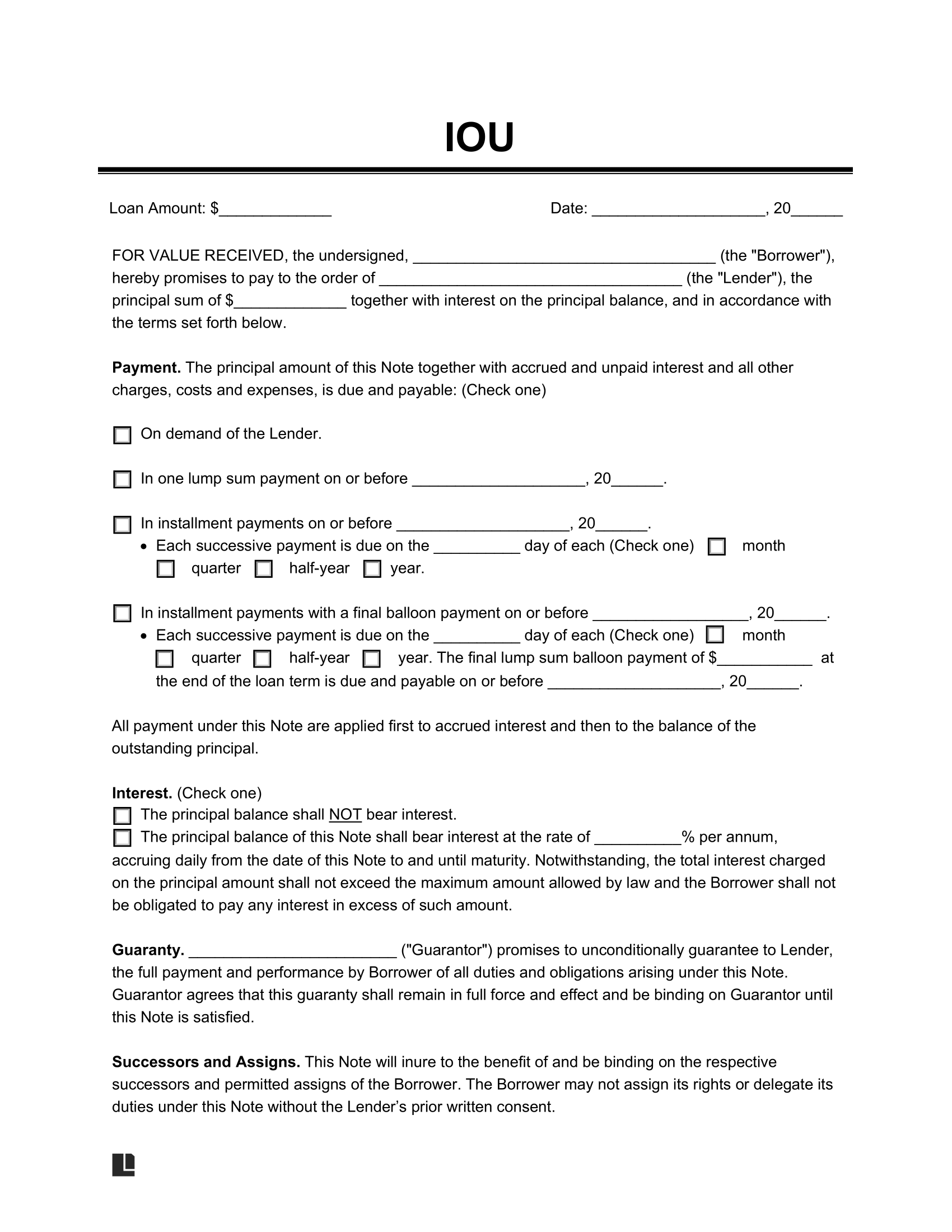

The first step is noting the basic information of the parties involved and the loan amount. Record the lender’s and borrower’s names and the title loan amount before applying interest.

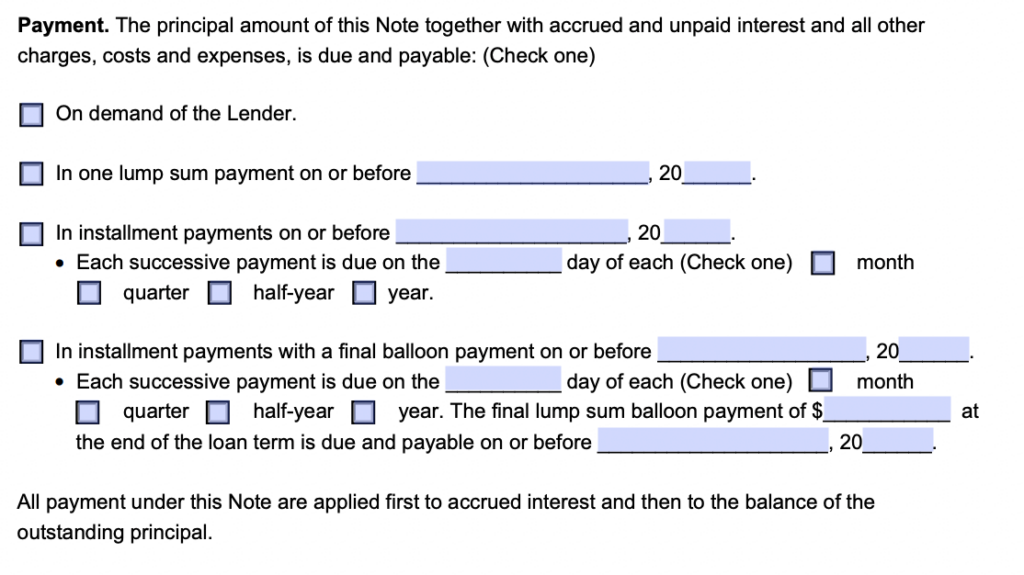

Detail how the borrower will pay back the IOU. There are multiple options available to the lender:

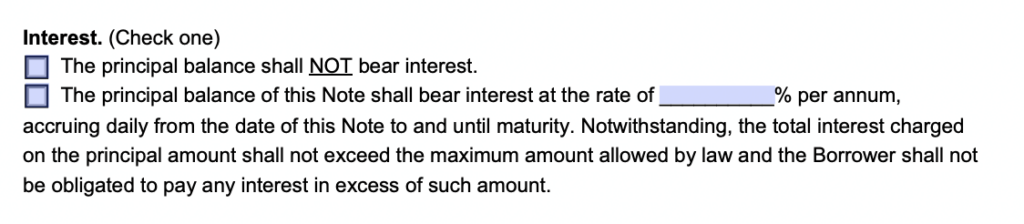

If you lend money to another party and would like to be compensated for giving a loan, you can specify that you would like the borrower to pay back the debt with accrued interest.

The maximum interest rate is governed by state law, so it is best to check your state for the maximum interest rate you can set in a loan transaction.

If you want assurance in receiving your money back, you can specify the borrower needing a cosigner or guarantor. If the borrower cannot find one, they will be fully responsible for paying back the loan.

To further protect both parties, you should include terms including but not limited to the following:

Write down your resident state. Remember that in the event of a dispute, the court will proceed under the state’s laws noted in the IOU unless the parties agree to another governing jurisdiction.

Include the signatures of all parties involved. If there is a cosigner or guarantor, they must include their signature too.

Learn about the differences between an IOU, promissory note, and loan agreement below:

| Aspect | IOU | Promissory Note | Loan Agreement |

|---|---|---|---|

| Complexity | The most informal and least complex of the three. | It's more formal and complex than an IOU but less formal and complex than a loan agreement. | The most formal and complex of the three. |

| Content | It describes the amount owed and includes the borrower's signature. It may have other elements depending on the parties' attention to detail. | It typically includes the borrowed sum, interest rate, repayment date, and the borrower's signature. | In addition to the details in a promissory note, a loan agreement also contains information about the collateral (if applicable), default terms, and other legal provisions. |

| Legal Enforceability | It's the most challenging to enforce in court because of its ambiguity. | It's typically enforceable in court. | It's the easiest to enforce in court because of its detailed nature. |

| Use Cases | It's most common for individuals to use this document when loaning small sums to family and friends. | Individuals can use this document for business or personal loans. | Individuals and businesses use this document for mortgages or other more complex loan arrangements that involve larger sums of borrowed money. |

Download an I Owe You template in PDF or Word format below:

Create Your IOU in Minutes!